For the past 52 years, Harold Averkamp (CPA, MBA) has worked as an accounting supervisor, manager, consultant, university instructor, and innovator in teaching accounting online. He is the sole author of all the materials on AccountingCoach.com.

![]()

Author:

Harold Averkamp, CPA, MBA

How Net Income Affects Stockholders' Equity, Statement of Comprehensive Income, How Other Comprehensive Income Affects Stockholders' Equity, Additional Information Regarding the Income Statement, Income Statements That Remain Inside the Company

Did you know? You can earn our Income Statement Certificate of Achievement when you join PRO Plus. To help you master this topic and earn your certificate, you will also receive lifetime access to our premium financial statements materials. These include our video training, visual tutorial, flashcards, cheat sheet, quick tests, quick test with coaching, business forms, and more.

When you join PRO Plus, you will receive lifetime access to all of our premium materials, as well as 11 different Certificates of Achievement.

The income statement is one of the main financial statements of a business. Other names for the income statement include:

The income statement reports revenues, expenses, gains, losses, and the resulting net income which occurred during the accounting period shown in its heading. Typical periods or time intervals covered by an income statement include:

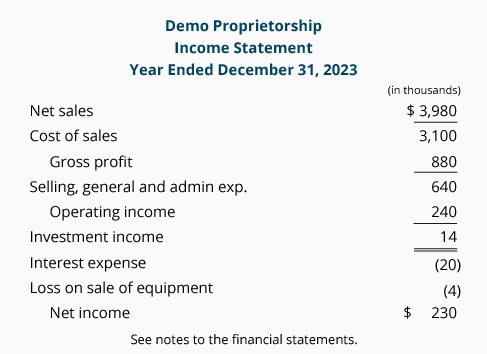

The following is an outline of an income statement for a regular U.S. corporation:

Below are additional details for the lines in Example Corporation’s income statement:

Operating revenues are the amounts earned from the company’s main business activities. Common operating revenues are:

Operating expenses are the expenses associated with the company’s main business activities. Common operating expenses include:

Operating income is the result of subtracting the company’s operating expenses from its operating revenues.

Nonoperating revenues or income, nonoperating expenses, gains, and losses result from activities outside of the company’s main business activities. Common examples for retailers and manufacturers include investment income, interest expense, and the gain or loss on the sale of equipment that had been used in the business.

Income before income tax expense is the combination of the amount of operating income and the nonoperating amounts.

Income tax expense is the federal, state, and local income taxes relating to the amounts appearing on the income statement. (The actual amount paid will likely be different, since the amount paid is based on the amounts on the corporation’s income tax returns.)

Net income is the amount of earnings remaining after subtracting the income tax expense.

Notes to the financial statements refers the reader to important information that could not be communicated by the amounts shown on the face of the income statement.

Note:

If a corporation’s shares of common stock are traded on a stock exchange, the earnings per share and the average number of shares outstanding must also be shown on the income statement.

Additional details and examples of income statements will be provided later.

Please let us know how we can improve this explanation

Submit Feedback No ThanksNet sales is the gross amount of Sales minus Sales Returns and Allowances, and Sales Discounts for the time interval indicated on the income statement.

Under the accrual basis of accounting, the Service Revenues account reports the fees earned by a company during the time period indicated in the heading of the income statement. Service Revenues include work completed whether or not it was billed. Service Revenues is an operating revenue account and will appear at the beginning of the company’s income statement.

Also referred to as SG&A. For a manufacturer these are expenses outside of the manufacturing function. (However, interest expense and other nonoperating expenses are not included; they are reported separately.) These expenses are not considered to be product costs and are not allocated to items in inventory or to cost of goods sold. Instead these expenses are reported on the income statement of the period in which they occur. These expenses are sometimes referred to as operating expenses.

Income or revenue earned by a company that is outside of its main operating activities. For a retailer the interest earned on its temporary investments is a nonoperating revenue (or nonoperating income).

An expense outside of a company’s main operating activities of buying and selling merchandise or providing services. For example, interest expense is a nonoperating expense.

This is the bottom line of the income statement. It is the mathematical result of revenues and gains minus the cost of goods sold and all expenses and losses (including income tax expense if the company is a regular corporation) provided the result is a positive amount. If the net amount is a negative amount, it is referred to as a net loss.